Why Your Credit Score Matters When Applying for Car Finance

When you apply for car finance, your credit score can play a big part in the finance you’re offered. It can affect whether you’re accepted, which lenders are available to you and the interest rate you may be charged.

When you apply for car finance, your credit score can play a big part in the finance you’re offered. It can affect whether you’re accepted, which lenders are available to you and the interest rate you may be charged.

But your credit score isn’t the only thing lenders look at. Many finance providers will also consider your income, employment status, affordability, existing commitments and the vehicle you want to finance.

In this guide, we’ll explain what your credit score is, how it’s calculated, what can affect it, how to improve it and why a better credit profile could get you better car finance rates.

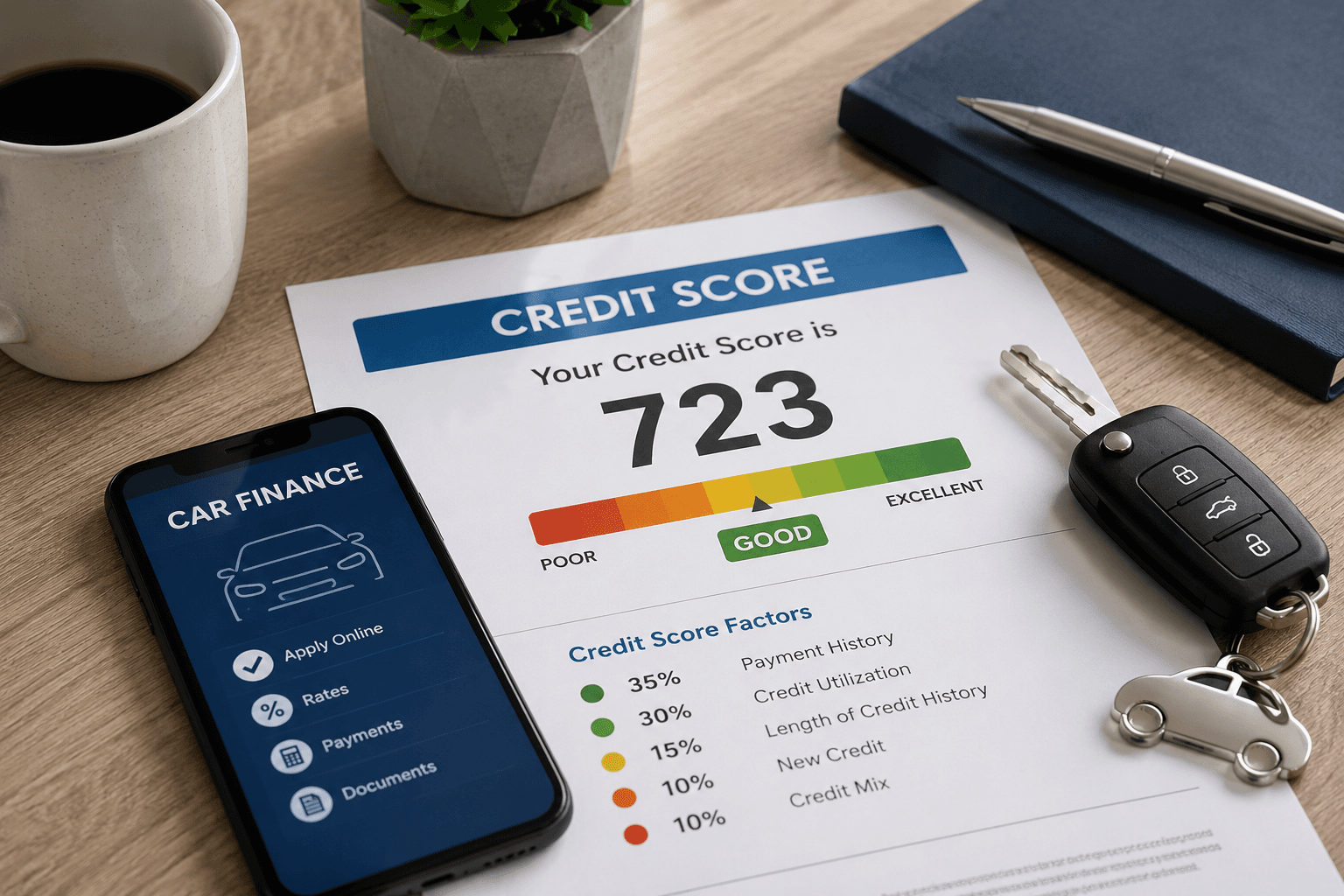

What Is a Credit Score?

A credit score is a number that shows how you’ve managed credit in the past. It gives lenders an idea of whether you’ll repay the money you borrow.

In the UK, there is no single universal credit score. The main credit reference agencies, Experian, Equifax and TransUnion, each use their own scoring systems. So your score may be different depending on where you check it.

Your credit score is based on the information in your credit report. This can include loans, credit cards, mobile phone contracts, mortgages, missed payments, defaults, County Court Judgments and previous credit applications.

For car finance lenders, the score itself is useful, but your wider credit history matters more. A lender will want to know your overall financial behaviour, not just one number.

How Is Your Credit Score Calculated?

Your credit score is calculated using several factors from your credit report. One of the most important is your payment history. If you make regular repayments on time, this shows lenders you’re reliable. Missed or late payments can have the opposite effect and remain on your credit file for up to 6 years.

Credit utilisation is another key factor. This is how much of your available credit you’re using. For example, if you have a credit card with a £2,000 limit and you owe £1,800, you’re using a high percentage of your available credit. Lenders may see this as a sign you’re relying too much on borrowing.

The length of your credit history can also make a difference. If you’ve managed credit well for several years, this can work in your favour. Someone with very little credit history may find it harder for lenders to assess their reliability. Lenders may also consider the types of credit you have used, how many recent applications you have made and if there are any serious issues in your file, such as defaults, CCJs, bankruptcy or IVAs.

What Can Damage Your Credit Score?

Your credit score can be affected by a range of financial behaviours. One of the most common causes of a lower score is missing payments on loans, credit cards, finance agreements or household bills.

Late payments can also have an impact, even if you eventually catch up. From a lender’s point of view, missing or late payments may suggest you could struggle to keep up with future finance repayments.

Using a large amount of your available credit can also reduce your score. If you’re regularly close to your credit limits, lenders may see this as a sign that your finances are under pressure.

Applying for lots of credit in a short period can also be harmful. Each hard credit search leaves a footprint on your credit report, and too many searches may make lenders cautious.

More serious credit issues, such as defaults, CCJs, IVAs or bankruptcy, can have a bigger effect. These don’t always mean you can’t get car finance, but they may reduce the number of lenders available to you or increase the interest rate you’re offered.

How Your Credit Score Affects Car Finance Rates

Your credit score can affect the car finance rates you’re eligible for because lenders use your credit profile to assess risk.

Generally, applicants with stronger credit histories are seen as lower risk. This can mean more lenders, higher approval chances and more competitive APRs.

Applicants with poor or limited credit histories may still be accepted, but they may be offered higher interest rates. This is because the lender is taking on more perceived risk.

A lower APR can make a big difference to the total amount you repay. Even if the monthly payment only changes the savings over a four or five-year finance agreement slightly, it could be substantial.

| Credit Profile | Possible Outcome |

|---|---|

| Excellent credit | Wider lender choice and more competitive rates |

| Good credit | Strong approval chances and reasonable APR options |

| Fair credit | Finance may be available, but rates may be higher |

| Poor credit | Specialist lenders may be needed and APR may be higher |

These examples are only a guide. The rate you are offered will depend on your individual circumstances, the lender, the vehicle, the deposit and the finance agreement.

Is Your Credit Score the Only Thing Lenders Look At?

No. Your credit score is important, but it’s only part of the decision.

Car finance lenders will also look at whether the agreement is affordable for you. This means they may consider your income, employment status, monthly outgoings, rent or mortgage payments, existing loans and other financial commitments.

They may also look at the amount you want to borrow, the value of the vehicle, the length of the agreement and whether you are paying a deposit.

This is why two people with similar credit scores can get different finance offers. A good credit score helps, but affordability is just as important.

Soft Credit Checks vs Hard Credit Checks

When applying for car finance, it’s useful to understand the difference between a soft credit check and a hard credit check.

A soft credit check allows a lender or broker to review your eligibility without affecting your credit score. It can help you see if you’ll be accepted before making a full application.

A hard credit check usually happens when you proceed with a formal finance application. This type of search is visible to other lenders and can affect your credit score, especially if you apply for several finance products in a short space of time.

carloans 365 uses an initial soft credit search, so you can check your finance options without damaging your credit score.

Can You Get Car Finance With Bad Credit?

Yes, you can get car finance with bad credit.

A poor credit score doesn’t mean you’ll be declined. Many lenders understand that people experience financial difficulties for different reasons, such as redundancy, illness, relationship changes or unexpected expenses.

You may still be considered if you’ve missed payments, defaults, CCJs, limited credit history or a low credit score. However, your options may be more limited, and the interest rate may be higher than that of someone with excellent credit.

Working with a broker like carloans 365 can help because your application can be matched with lenders who are more likely to consider your circumstances.

How to Improve Your Credit Score Before Applying for Car Finance

Improving your credit score takes time, but there are practical steps you can take before applying for car finance.

Make sure all bills and repayments are paid on time. Setting up Direct Debits can help you avoid missed payments and build a stronger repayment history.

Also, check you’re registered on the electoral roll at your current address. This helps lenders verify your identity and can support your credit profile. Paying off existing debt can also help. If you can reduce your credit card balances or pay down outstanding borrowing, lenders may see you as less financially stretched.

Try not to make several credit applications before applying for car finance. Multiple hard searches in a short space of time can make lenders cautious.

Finally, check your credit report for errors. Incorrect addresses, outdated account information or unfamiliar accounts can affect your score. If you spot a mistake, contact the credit reference agency and ask them to correct it.

Common Credit Score Myths

One common myth is that checking your own credit score will damage it. This is not true. Checking your own report is classed as a soft search and does not affect your score.

Another myth is that bad credit means automatic rejection. While a poor credit history can make finance more challenging, it doesn’t always mean rejection. Some lenders specialise in helping people with adverse credit.

Some people also believe you need a perfect score to get car finance. In reality, many applicants are accepted with average or imperfect credit, as long as the finance is affordable, and the lender is happy with the overall application.

It’s also worth knowing that being declined by one lender doesn’t mean every lender will say no. Different lenders use different criteria, which is why using a broker can be helpful.

How Your Credit Score Affects Your Car Finance Application

Your credit score matters when applying for car finance, but it doesn’t tell the whole story. Lenders look at your wider financial situation, including affordability, income, employment and existing commitments.

A better credit score can improve your chances of approval and may get you lower car finance rates. However, even if your credit history isn’t perfect, finance may still be available.

carloans 365 can help you check your options with an initial soft credit search, so you can see if you’ll be accepted without damaging your credit score.

Apply with carloans 365 today and find out what car finance options are available to you.